beijingwalker

ELITE MEMBER

- Joined

- Nov 4, 2011

- Messages

- 65,191

- Reaction score

- -55

- Country

- Location

Chinese LNG whispers send European gas markets into jitters

Brittle EU gas markets were rattled by misplaced fears of renewed Chinese appetite for LNG. In fact, China barely needs spot LNG and will probably be sending more cargoes to Europe in the coming years

Seb Kennedy

March 14 2023

Europe, we are told, should fear China. A prevailing narrative in some energy circles is that post-Covid Chinese demand for liquefied natural gas will come roaring back and that Europe will face a much tougher task restocking gas for next winter than last time around.

The narrative is not entirely incorrect but it certainly says more about the current energy situation in Europe than China. To better understand this dynamic, Energy Flux takes a look at structural shifts underway in China’s gas market. If you’re pressed for time here’s a quick overview:

- EU gas prices spiked on misplaced fears of renewed Chinese appetite for LNG

- China barely needs any more LNG and is replacing Europe as global swing demand market

- Plummeting Chinese LNG terminal utilisation points to structural excess and more cargo diversions

- EU deindustrialisation poses a small tail risk to Chinese LNG portfolio length over the long term

Misplaced fears

The European benchmark gas contract, Dutch TTF, last week spiked 20%. The surprise upward move, following weeks of successive declines, was ascribed to a mix of French strikes shutting refineries and LNG terminals, fresh concerns over France’s nuclear fleet, a late cold snap and – yes – signs of incipient recovery in Chinese LNG demand.Pre-Ukraine, these events in aggregate would not warrant a spasmodic surge in TTF back to €53/MWh (~$14/MMBtu). With Europe still traumatised by the loss of cheap Russian gas, markets are very much on edge – even when EU gas stocks are at record highs for this time of year and racing towards tank-tops.

Chinese demand is certainly not ‘roaring’ back – at least, not yet. So far, there have been only tepid forays into spot procurement by state giant CNOOC and one or two smaller independent players. But the potential for that to change keeps EU gas markets jittery.

The International Energy Agency says China’s return to the spot market now poses a bigger threat to European gas balances than a complete cessation of (what little remains of) Russian gas flows into the EU. The IEA forecasts China’s LNG demand to reach 94 billion cubic metres (Bcm) in 2023, with a large delta of uncertainty skewed to the upside.

Sensitivity analysis by the IEA concluded that a confluence of “moderately bearish” factors would depress China’s LNG intake by just 12% (10 Bcm) in 2023, whereas “moderately bullish” conditions would boost imports by 35% (30 Bcm) to 115 Bcm – well above the previous peak in 2021.

That’s a big delta: 40 Bcm represents about 29 million tonnes of LNG, or roughly 7% of total global LNG trade in 2022. The spot market, and hence the affordability of gas in Europe and almost all gas-importing countries, is at the whim of the vagaries of China’s post-Covid economic performance.“The total uncertainty range is about 40 Bcm, with China’s 2023 net imports reaching 75 bcm at the low end and 115 bcm at the high end. This range is greater than the uncertainty associated with the potential loss of all remaining pipeline gas flows into Europe from Russia, which have averaged about 28 bcm on an annualised basis since deliveries via the Nord Stream 1 pipeline were cut off indefinitely at the end of August 2022.” – IEA

In the IEA’s central case Chinese LNG imports grow by 8 Bcm (+10%) this year compared to 2022. Trade publication Energy Intelligence is less bullish, forecasting import growth of 4.1 Bcm in 2023. In either case this represents only a partial recovery, since demand crashed by an unprecedented 22 Bcm (-21%) last year amid high spot prices, slowing economic growth and zero-Covid lockdowns that are now being lifted.

Share

No need for more LNG

Chinese demand is only one element of the ‘threat to Europe’ equation. Contracts and prices also matter. This is where things get interesting.

China is a price-sensitive gas market and LNG is a marginal fuel. Absent a state mandate from Beijing to buy up cargoes ‘at any cost’ (as occurred in winter 2021), incremental demand softens when spot prices rise above long-term contracts. This is precisely what happened in 2022, with contracts assessed at about 30% below spot.Beijing read the runes when gas markets tightened suddenly in summer 2021. With pre-war tensions rising in Ukraine, China went on a spectacular LNG buying spree. State-run importers such as PetroChina signed a slew of long-term contracts to insulate themselves against the coming period of spot market volatility. A sizeable chunk will come from US liquefaction projects, which offer destination flexibility as standard.

The first of those contracts are now kicking in, with about 13 Bcm of new supply starting delivery in 2023. That will bring China’s contracted LNG volume to nearly 110 Bcm this year. Per the IEA, this means China could in 2023 “ramp up its LNG imports back to 2021 levels without the need to increase spot LNG purchases”.

That’s wild. Instead of competing for spot cargoes, China can simply leverage its control of the market. In very crude terms, the calculus at PetroChina or Sinopec could go something along the lines of: post-Covid infections closing ports and factories? No problem, divert contracted cargoes to wherever they can fetch the best netback. Economic reopening off the charts? Let the LNG flow in, fire up the regasifiers!

Flexibility = power

Europe was for years the ‘market of last resort’ for LNG, mopping up spare cargoes during periods of oversupply and forsaking imports when Asian demand spiked. Now those roles are reversing.War is depriving Europe of its traditional role of gas demand swing market, and a maturing China is taking up that mantle. The two main drivers of this shift are a cessation of Russian gas flows and China’s evolution beyond the LNG growth market phase.

The former is well understood, the latter less so. Structural changes underway in China’s gas sector can be broken down into three broad categories:

- More non-LNG gas in China’s domestic energy mix (i.e. domestic production and pipeline imports)

- Rapid growth in Chinese LNG regasification and storage capacity

- More renewables, nuclear and coal generation in Chinese power mix

1. More molecules, same market

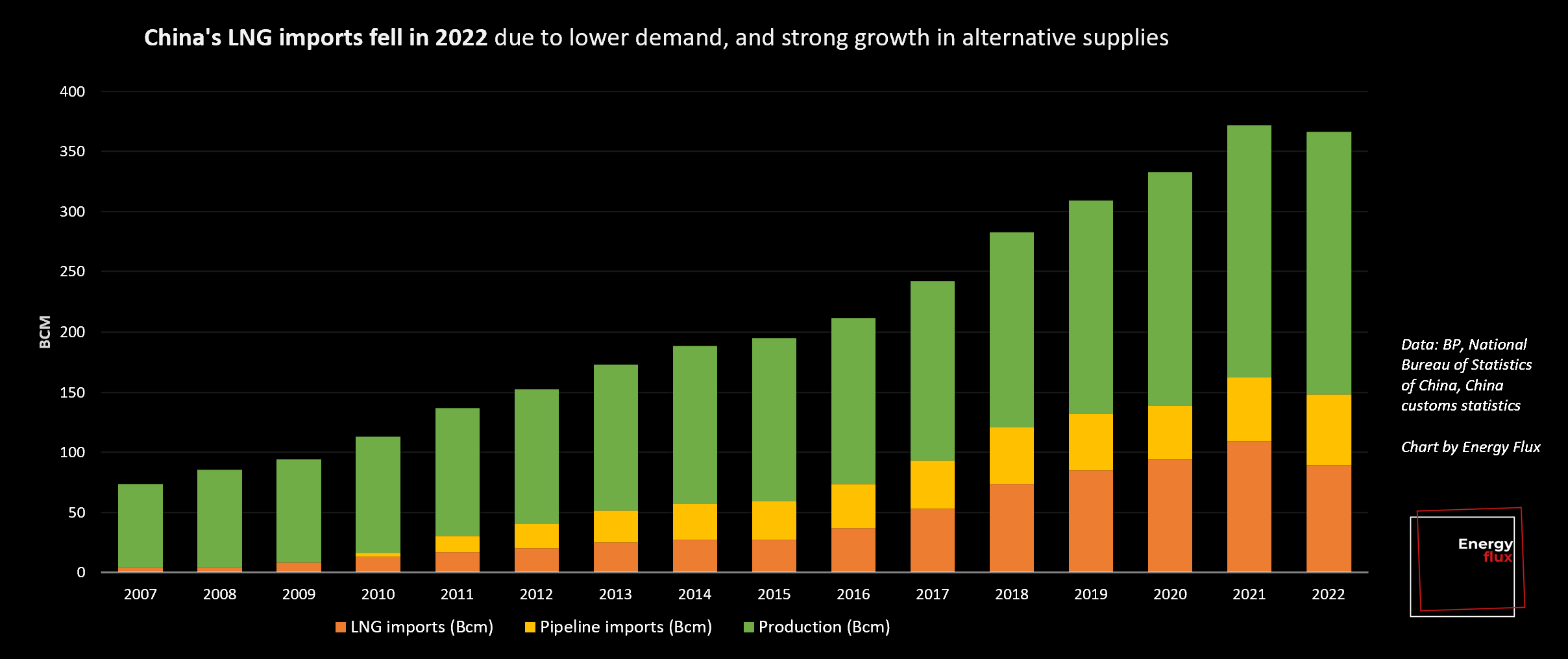

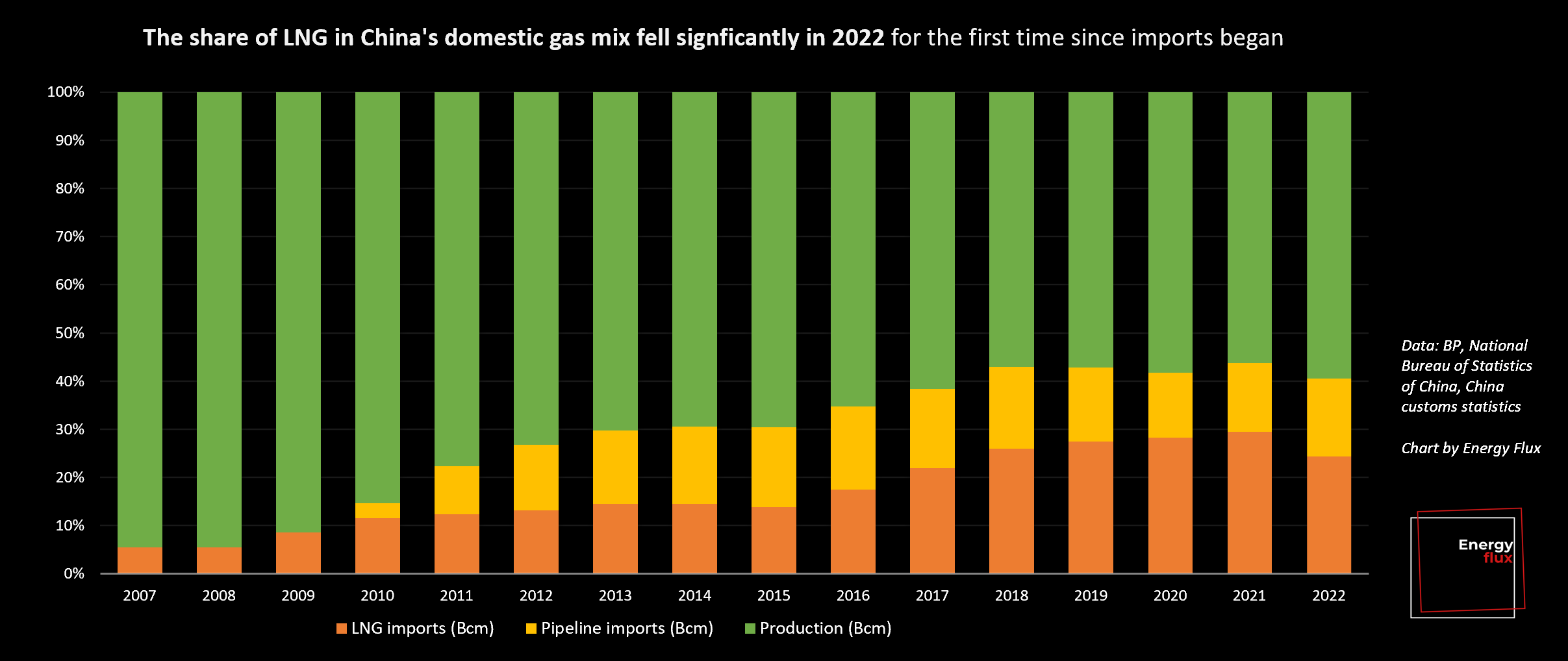

After 15 consecutive years of rip-roaring growth, China’s LNG imports slammed into reverse in 2022 and fell by almost one-fifth to 89 Bcm. But overall gas consumption fell by less than 2%, because other sources took up the slack. China’s domestic gas production rose to 218 Bcm (+12%) in 2022, accelerating a trend of firm production growth (+7% over 2011-2021). And pipeline imports grew to 59 Bcm (+4%) driven by increased eastwards flows from Russia.

In terms of market share, LNG has been a disruptor in China’s gas mix. But last year LNG was itself disrupted by exogenous market events and strong competition from non-LNG sources. Was 2022 a blip, or is China’s LNG import growth reaching a point of attrition?

2. Infrastructure overkill

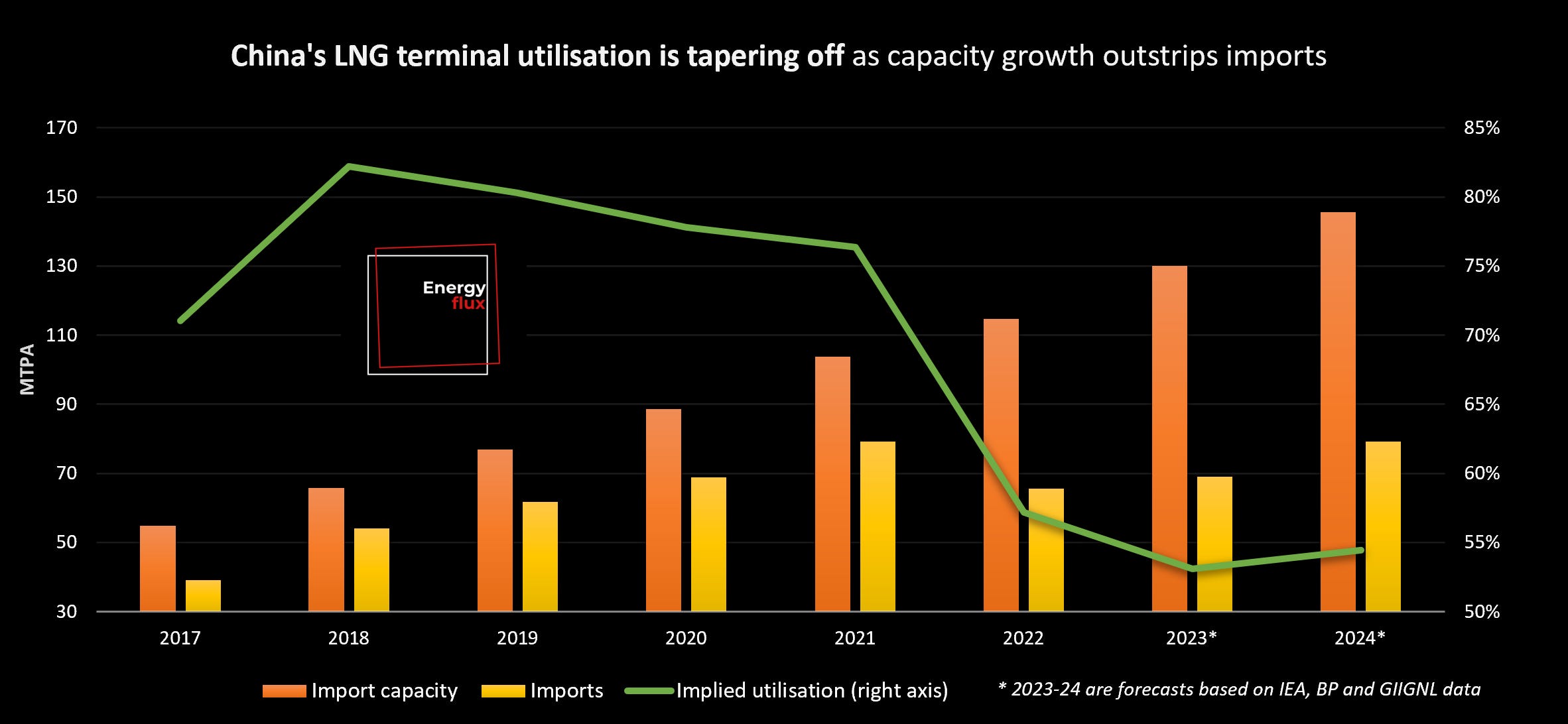

A necessary feature of Europe’s historic role as an LNG sink was chronically underutilised import infrastructure. Asian LNG demand has always been less elastic due to a relative lack of regasification and storage capacity. That remains the case today, but China seems to be following Europe’s ‘white elephants’ approach to gas infrastructure expansion: embracing over-capacity.To operate as an effective swing market for LNG, China needs enough import capacity to absorb contracted volumes over the duration of long-term contracts – and be happy to let much of it lie idle for weeks or months at a time, when market conditions require cargoes to be diverted away from China en masse.

Utilisation of Chinese terminals remains high by European standards, but that is changing. Regas and storage facility construction is booming, with more than 30 mtpa of capacity forecast to come online by 2024 just as LNG import growth goes soft. Utilisation rates peaked at 82% in 2018 and could fall as low as 53% depending on how much LNG ends up being consumed within China.

3. Squeezed out of the power mix

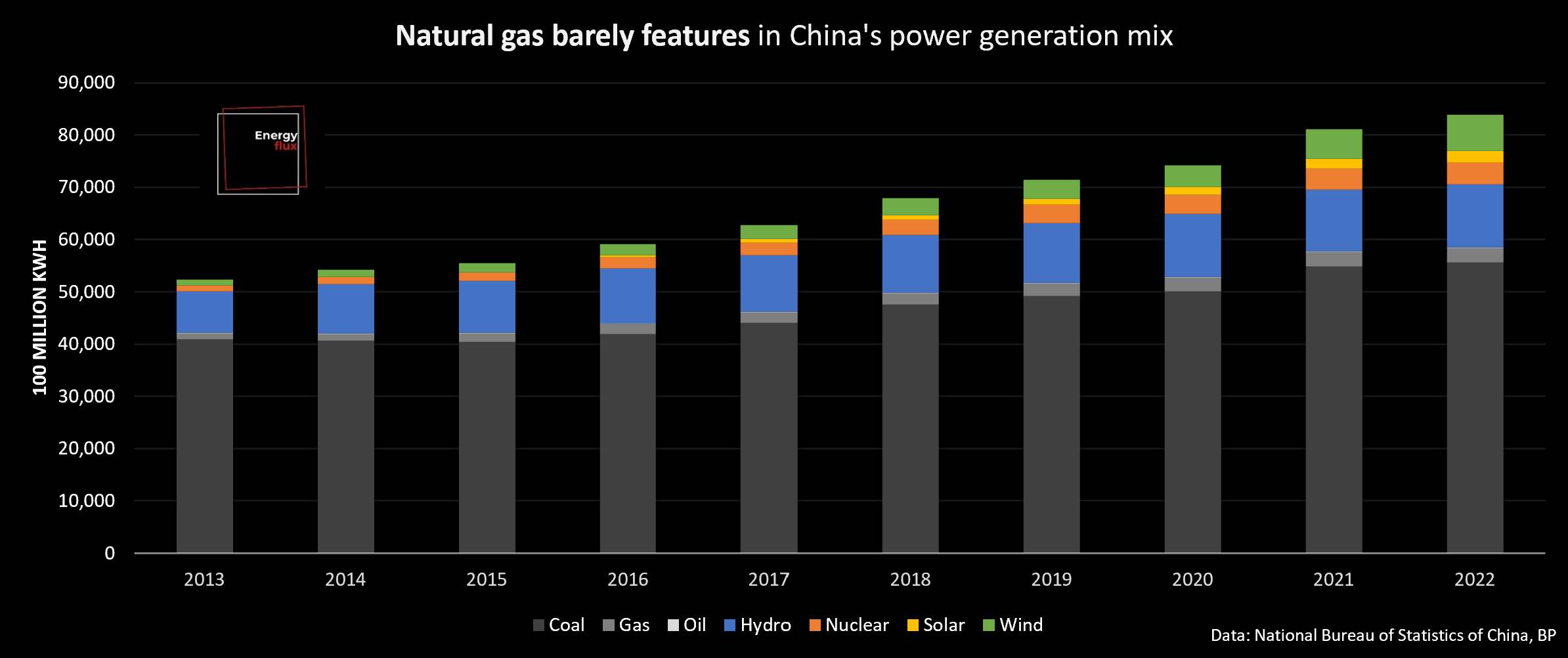

LNG is a premium fuel that must compete with cheaper domestic sources of power and heat. It is more expensive and difficult to store than coal, and relying on it to keep the lights on and stoves warm is a risky strategy. Just ask Pakistan, which endured load shedding and blackouts when LNG procured in spot markets failed to show up. Pakistan has now given up on spot procurement in favour of more domestic coal and renewables.China is also ramping up coal and renewable power and giving gas the cold shoulder. Wind generation overtook gas-fired power more than 10 years ago, and solar PV is poised to do the same this year or next. Gas barely features in the electricity mix, accounting for just 3% of generation in 2021. That won’t change soon: China’s thermal capacity expansions are entirely centred on coal, not gas.

The point here is that gas burn is structurally low in the Chinese power mix, meaning there is no baseload demand anchor to absorb all that new LNG that China has committed to buy. And with more non-LNG gas molecules competing for the same number of burner tips, there is potential for China to find itself in surplus even during periods of global gas market tightness.

Get original data-driven market analysis in your inbox. Subscribe for free or make a recurring donation to Energy Flux:

Caught short, or caught long?

This is all well and good when European economies are still leaning heavily on LNG while figuring out how to function without Russian gas. But that adjustment is happening quickly, with high prices driving alarming levels of deindustrialisation and demand reduction. All of this is dovetailing with resilient climate ambition and robust renewable energy expansion in Europe (and elsewhere).Add to the outlook the coming wave of new liquefaction plants scheduled to come onstream by 2026, and global LNG market tightness could rapidly loosen over the next three years. Uncorrelated swings in gas demand and LNG supply will put Asian spot prices and European gas hubs on a volatility rollercoaster.

Against this backdrop, China’s major state-run LNG importers will need to be ready to divert more cargoes at short notice, and have a back-up plan for when prices tank. Price-sensitive south Asian markets provide a floor, so holding regasification capacity in India could provide a strategic outlet for cargoes that are out of the money in Europe and surplus to requirements in China.

Risk perception and time horizons

With all this in mind, how should we view the ‘Europe must fear China’ narrative? Are some energy observers looking at the market through the wrong end of the telescope? Should China instead fear European demand destruction?The entire framing of the question could be wrong. In a sense, China is doing Europe a favour: signing long-term LNG supply contracts that European companies cannot reconcile with net zero targets. China is giving demand certainty to LNG projects, underwriting investment in new supplies that will periodically find their way into Europe (for a price).

In the near-term, Europe’s fragile energy situation certainly exposes it to a robust recovery in Chinese demand. But over a very long time horizon, the risk will gradually shift from regions short on gas to those over-committed to buying the most expensive form of the fuel: LNG. In this regard, portfolio length is a small but non-trivial tail risk for China.

In the medium-term, market imbalances will shift perceptions of risk between over and undersupply. Expect renewed calls for Europe to sign long-term US LNG supply contracts next winter when EU gas stocks are depleted and TTF is again spiralling skywards. Those same voices will fall silent when the world is awash with LNG in summer 2025 or 2026.

The challenge for market observers, investors and energy planners is to maintain perspective. It is easy to lose sight of the slow-burn transition trajectory as choppy markets plough through peaks and troughs in the energy cycle. Europe’s shift away from gas might be slow, but it is definitely happening.

Chinese whispers, European jitters

Brittle EU gas market rattled by misplaced fears of LNG demand recovery in China

www.energyflux.news

www.energyflux.news