Fieldmarshal

FULL MEMBER

- Joined

- Nov 10, 2010

- Messages

- 621

- Reaction score

- 0

- Country

- Location

Mobile Money Revolution: Pakistan Surges Ahead of India

Haq's Musings: Mobile Money Revolution: Pakistan Surges Ahead of India

Pakistan government is handing out Rs. 40,000 per family to nearly a million internally displaced persons (IDPs) through mobile service operator Zong's mobile SIMs. The government is attempting to ease the discomforts of displacement for such a large number of people displaced after the start of Pakistan Army's Operation ZarbeAzb to root out terrorists from North Waziristan tribal agency. Zong is one of several mobile service operators offering Easypaisa m-money service. It was pioneered by Telenor Pakistan.

Easypaisa moved $3.5 billion in fiscal 2012-13. Bangladesh's bKash did $4 billion over the same period. These figures were well ahead of the $3.2 billion moved in comparable period by India's M-Pesa mobile money network, according to New York Times. Over the last 12 months, the m-money market volume in Pakistan has reached 153 million annual transactions worth US$ 6.2 billion, according to Asian Development Bank.

Easypaisa M-money Growth in Pakistan (Source: ADB)

Pakistan’s m-money infrastructure has grown rapidly since the launch of the first domestic initiative in October 2009. This expansion has been enabled by a liberal financial and telecommunications regulatory framework, and active private sector participation. Four out of five cellular mobile companies currently operating in Pakistan have launched m-money systems in partnership with financial institutions. The m-money market volume has reached 153 million annual transactions worth US$ 6.2 billion.

There are two ways through which m-money services are offered in Pakistan. Over 95% of m-money transactions are done through mobile banking (m-banking) agents, and the rest are processed directly through customers’ mobile-wallet (m-wallet) accounts, using mobile phones. M-banking agents (retail points) provide the basic infrastructure for Pakistan’s m-money services, whereas customers’ m-wallet accounts currently have a limited role in the m-money services market.

It is believed that the reason why India lags behind Bangladesh and Pakistan in mobile money is because its regulators require mobile operators to work with banks to provide the services. Mobile networks would prefer to have their own agents who can cash out the digital money into hard currency. Much of the infrastructure is already in place, because there are so many locations where customers can top up on airtime. But the mobile operators are not allowed to use those sales outlets as financial agents in India.

As was reported below some years earlier....Pakistan is going from strength to strengh

Pakistan Ranks High in Microfinance

Haq's Musings: Pakistan Ranks High in Microfinance

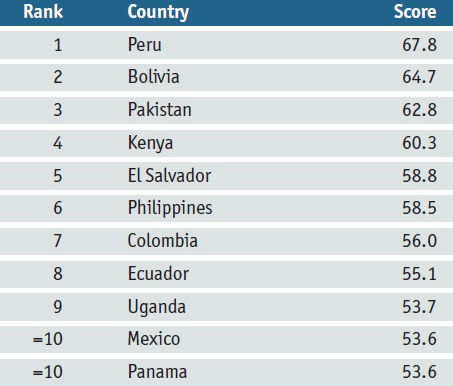

Pakistan ranks first in Asia and third in the world in Economist Intelligence Unit's overall microfinance business environment rankings for 2011. Among other Asian nations, only the Philippines at #6 made the top ten list.

On a scale of 0-100, Pakistan scores 62.8, just behind top-ranked Peru's 67.8 and second-ranked Bolivia's 64.7 in overall global rankings of 55 countries. Among nations in South Asia region, India ranks 27 with a score of 43.1 and Bangladesh ranks 43 with a score of 30.9. Sri Lanka is at #48 with a score of 27.4 followed by Nepal at 51 scoring 26.1.

Among various categories, Pakistan ranks #1 in regulatory framework and practices and #5 in supporting institutional framework.

Here's an excerpt on Asia from the EIU report titled "Global microscope on the microfinance business environment":

"Pakistan and the Philippines again top the regional rankings for East and South Asia. These countries both finished in the top ten globally, signifying strong environments for microfinance. Indeed, Pakistan and the Philippines came first and second globally, respectively, in the Regulatory Framework and Practices category, suggesting strong regulatory regimes and good prospects for MFIs to enter the sector and perform effectively. The Philippines, for example, has had a strong enabling environment for microfinance for more than a decade. Cambodia is third best in Asia and makes it into the top 25% globally. India comes next, but fell precipitously after the crisis that struck the sector last year. Mongolia finished fourth in Asia, but was the region’s most-improved performer."

Recently, Pakistan's central bank governor Haris Anwar said that large segments the nation's population have no bank accounts and many do not understand why it puts them at a disadvantage when it comes to their personal financial management. According to Pakistan Access to Finance Survey (A2FS), only 12 percent of the population has access to formal financial services. Of the remaining 88 percent, only 32 percent are informally served and 56 percent are completely excluded, Anwar said, adding that according to the A2FS analysis, about 40 percent of the financially excluded population reported lack of understanding of financial products as the main reason for financial exclusion.

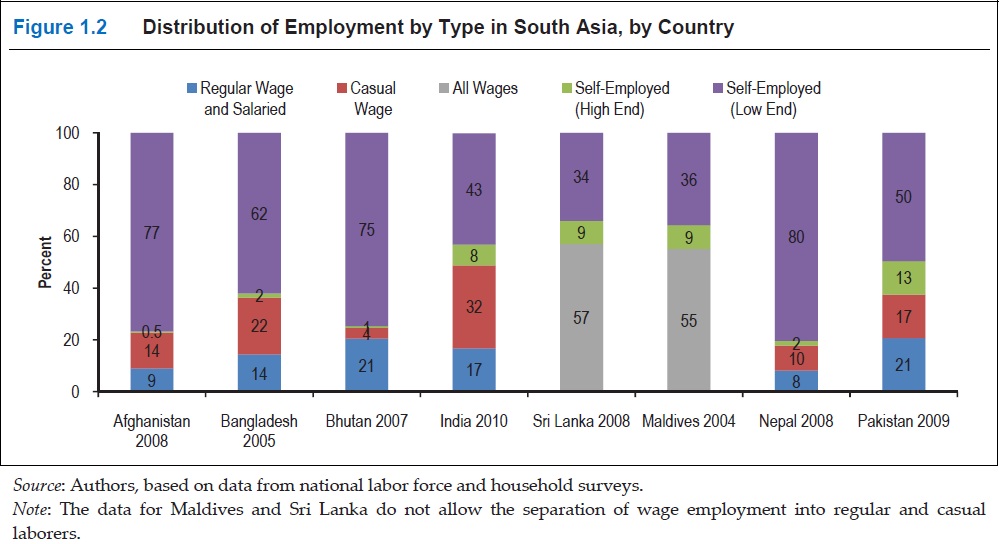

It has long been recognized by poverty alleviation experts that pursuing policies for increasing financial inclusion, such as encouraging microfinance, are absolutely essential to lift tens of millions of people out of poverty in Pakistan, where 50% of the workforce is made up of low-end self-employed. Other efforts toward bringing financial services to the poor and lower middle class in Pakistan include financial literacy initiatives and growth of branchless mobile banking in city slums and rural areas of the country.

Pakistan’s first-ever National Financial Literacy Program was launched earlier this year with the support and collaboration of Asian Development Bank (ADB), Pakistan Banks’ Association (PBA), Pakistan Microfinance Network (PMN), Pakistan Poverty Alleviation Fund (PPAF) and BearingPoint consultants.

The growth of branchless banking in Pakistan is now being held up a success story at international fora. Within a span of just two years, there are now almost 18,000 branchless banking outlets surpassing the 10,000 conventional bank branches, according to Governor Anwar. UBL Omni’s branchless banking service launched in April 2010 by United Bank has won several contracts to disburse payments for nongovernment organizations and government schemes to help those affected by floods. UBL reports that at the end of June it had 5,000 agents disbursing payments to 2 million recipients under these programs. UBL Omni has also started accepting loan repayments for microfinance institutions (MFIs) and providing cash management facilities for businesses.

According to a recent World Bank report titled "More and Better Jobs in South Asia" which shows that 63% of Pakistan's workforce is self-employed, including 13% high-end self-employed. Salaried and daily wage earners make up only 37% of the workforce. Access to money is necessary for many of these entrepreneurs to succeed in realizing their dreams.

The history ofmicrofinance in Pakistanstarted with the launch ofOrangi Pilot Project(OPP) in Kutchi Abadies (shanty towns) of Karachi in early 1980’s, according to a paper published by Abdul Qayyum and Munir Ahmed. In the late 1960s, prior to OPP, a few NGOs in the rural areas of Pakistan began to experiment with microcredit by offering subsidized loans. However, they mostly failed to reach the poor due to abuse and corruption. Now there are dozens of Micro Finance Institutions working in Pakistan. The MFIs in Pakistan can be divided into different groups based on their uniqueness that separates them from other financial institutions and makes them similar in terms of the way they function.

The first group consists of financial institutions with microfinance as a separate product line. The share of microfinance related activities of these institutions is up to 10 percent. This group includes Orix Leasing and the Bank of Khyber –both are profit making organizations and consider microfinance as a separate product line.

The second group refers to the specialized MFI’s, which includes two microfinance banks - The Khushhali Bank and First Microfinance Bank Limited (FMBL) - and two NGOs - KASHF Foundation and Asasah. All these institutions completely focus on provision of financial services and also have commercial focus as well.

Third category MFIs related to activities of the Rural Support Programs which deals with integrated Rural Development Programs with microfinance as one of its activities. These organizations are National Rural Support Programs (NRSP), Punjab Rural Support Programs (PRSP) and Sarhad Rural Support Programs (SRSP). The last group consists of private NGOs. These NGOs are basically integrated development organizations with microfinance as one of their activities. These include Orangi Pilot Project, Sungi Foundation, Taraqee Foundation, Development Action for Mobilization and Emancipation (TRDP), Sindh Agricultural & Forestry Workers Coordinating Organization (SAFWCO) and Development Action for Mobilization and Emancipation (DAMEN), among others.

Khushhali Bank was established in August 2000 as part of the Government of the Islamic Republic of Pakistan's Poverty Reduction Strategy. The Pakistan Microfinance Sector Development Program (MSDP) was developed with the technical assistance and funding of the Asian Development Bank, which provided a US$150 million loan to the government of Pakistan, US$70 million being used for micro-loans provided by KB. Headquartered in Islamabad, KB operates under the central bank's supervision (State Bank of Pakistan) with several commercial banks operating as its primary shareholders.

To broaden access, there are now efforts underway to offer Shariah-compliant microfinance products to those who are reluctant to participate in interest-based banking. Farz Foundation is among the first to do so. It is engaged in Islamic micro-financing for livestock and agriculture among the rural poor.

Pakistan has a long way to go to achieve financial inclusion for the majority of its population. The current efforts on increasing access to money for the poor are a good start on a long journey that may take decades to complete. My readers who are interested in helping the poor in Pakistan by offering small loans of $25 or more have a choice of many websites to do so, including kiva.org which I have been using. The loans to Pakistani recipients are administered through Asasah, a Kiva partner in the country.

Haq's Musings: Mobile Money Revolution: Pakistan Surges Ahead of India

Pakistan government is handing out Rs. 40,000 per family to nearly a million internally displaced persons (IDPs) through mobile service operator Zong's mobile SIMs. The government is attempting to ease the discomforts of displacement for such a large number of people displaced after the start of Pakistan Army's Operation ZarbeAzb to root out terrorists from North Waziristan tribal agency. Zong is one of several mobile service operators offering Easypaisa m-money service. It was pioneered by Telenor Pakistan.

Easypaisa moved $3.5 billion in fiscal 2012-13. Bangladesh's bKash did $4 billion over the same period. These figures were well ahead of the $3.2 billion moved in comparable period by India's M-Pesa mobile money network, according to New York Times. Over the last 12 months, the m-money market volume in Pakistan has reached 153 million annual transactions worth US$ 6.2 billion, according to Asian Development Bank.

Easypaisa M-money Growth in Pakistan (Source: ADB)

Pakistan’s m-money infrastructure has grown rapidly since the launch of the first domestic initiative in October 2009. This expansion has been enabled by a liberal financial and telecommunications regulatory framework, and active private sector participation. Four out of five cellular mobile companies currently operating in Pakistan have launched m-money systems in partnership with financial institutions. The m-money market volume has reached 153 million annual transactions worth US$ 6.2 billion.

There are two ways through which m-money services are offered in Pakistan. Over 95% of m-money transactions are done through mobile banking (m-banking) agents, and the rest are processed directly through customers’ mobile-wallet (m-wallet) accounts, using mobile phones. M-banking agents (retail points) provide the basic infrastructure for Pakistan’s m-money services, whereas customers’ m-wallet accounts currently have a limited role in the m-money services market.

It is believed that the reason why India lags behind Bangladesh and Pakistan in mobile money is because its regulators require mobile operators to work with banks to provide the services. Mobile networks would prefer to have their own agents who can cash out the digital money into hard currency. Much of the infrastructure is already in place, because there are so many locations where customers can top up on airtime. But the mobile operators are not allowed to use those sales outlets as financial agents in India.

As was reported below some years earlier....Pakistan is going from strength to strengh

Pakistan Ranks High in Microfinance

Haq's Musings: Pakistan Ranks High in Microfinance

Pakistan ranks first in Asia and third in the world in Economist Intelligence Unit's overall microfinance business environment rankings for 2011. Among other Asian nations, only the Philippines at #6 made the top ten list.

On a scale of 0-100, Pakistan scores 62.8, just behind top-ranked Peru's 67.8 and second-ranked Bolivia's 64.7 in overall global rankings of 55 countries. Among nations in South Asia region, India ranks 27 with a score of 43.1 and Bangladesh ranks 43 with a score of 30.9. Sri Lanka is at #48 with a score of 27.4 followed by Nepal at 51 scoring 26.1.

Among various categories, Pakistan ranks #1 in regulatory framework and practices and #5 in supporting institutional framework.

Here's an excerpt on Asia from the EIU report titled "Global microscope on the microfinance business environment":

"Pakistan and the Philippines again top the regional rankings for East and South Asia. These countries both finished in the top ten globally, signifying strong environments for microfinance. Indeed, Pakistan and the Philippines came first and second globally, respectively, in the Regulatory Framework and Practices category, suggesting strong regulatory regimes and good prospects for MFIs to enter the sector and perform effectively. The Philippines, for example, has had a strong enabling environment for microfinance for more than a decade. Cambodia is third best in Asia and makes it into the top 25% globally. India comes next, but fell precipitously after the crisis that struck the sector last year. Mongolia finished fourth in Asia, but was the region’s most-improved performer."

Recently, Pakistan's central bank governor Haris Anwar said that large segments the nation's population have no bank accounts and many do not understand why it puts them at a disadvantage when it comes to their personal financial management. According to Pakistan Access to Finance Survey (A2FS), only 12 percent of the population has access to formal financial services. Of the remaining 88 percent, only 32 percent are informally served and 56 percent are completely excluded, Anwar said, adding that according to the A2FS analysis, about 40 percent of the financially excluded population reported lack of understanding of financial products as the main reason for financial exclusion.

It has long been recognized by poverty alleviation experts that pursuing policies for increasing financial inclusion, such as encouraging microfinance, are absolutely essential to lift tens of millions of people out of poverty in Pakistan, where 50% of the workforce is made up of low-end self-employed. Other efforts toward bringing financial services to the poor and lower middle class in Pakistan include financial literacy initiatives and growth of branchless mobile banking in city slums and rural areas of the country.

Pakistan’s first-ever National Financial Literacy Program was launched earlier this year with the support and collaboration of Asian Development Bank (ADB), Pakistan Banks’ Association (PBA), Pakistan Microfinance Network (PMN), Pakistan Poverty Alleviation Fund (PPAF) and BearingPoint consultants.

The growth of branchless banking in Pakistan is now being held up a success story at international fora. Within a span of just two years, there are now almost 18,000 branchless banking outlets surpassing the 10,000 conventional bank branches, according to Governor Anwar. UBL Omni’s branchless banking service launched in April 2010 by United Bank has won several contracts to disburse payments for nongovernment organizations and government schemes to help those affected by floods. UBL reports that at the end of June it had 5,000 agents disbursing payments to 2 million recipients under these programs. UBL Omni has also started accepting loan repayments for microfinance institutions (MFIs) and providing cash management facilities for businesses.

According to a recent World Bank report titled "More and Better Jobs in South Asia" which shows that 63% of Pakistan's workforce is self-employed, including 13% high-end self-employed. Salaried and daily wage earners make up only 37% of the workforce. Access to money is necessary for many of these entrepreneurs to succeed in realizing their dreams.

The history ofmicrofinance in Pakistanstarted with the launch ofOrangi Pilot Project(OPP) in Kutchi Abadies (shanty towns) of Karachi in early 1980’s, according to a paper published by Abdul Qayyum and Munir Ahmed. In the late 1960s, prior to OPP, a few NGOs in the rural areas of Pakistan began to experiment with microcredit by offering subsidized loans. However, they mostly failed to reach the poor due to abuse and corruption. Now there are dozens of Micro Finance Institutions working in Pakistan. The MFIs in Pakistan can be divided into different groups based on their uniqueness that separates them from other financial institutions and makes them similar in terms of the way they function.

The first group consists of financial institutions with microfinance as a separate product line. The share of microfinance related activities of these institutions is up to 10 percent. This group includes Orix Leasing and the Bank of Khyber –both are profit making organizations and consider microfinance as a separate product line.

The second group refers to the specialized MFI’s, which includes two microfinance banks - The Khushhali Bank and First Microfinance Bank Limited (FMBL) - and two NGOs - KASHF Foundation and Asasah. All these institutions completely focus on provision of financial services and also have commercial focus as well.

Third category MFIs related to activities of the Rural Support Programs which deals with integrated Rural Development Programs with microfinance as one of its activities. These organizations are National Rural Support Programs (NRSP), Punjab Rural Support Programs (PRSP) and Sarhad Rural Support Programs (SRSP). The last group consists of private NGOs. These NGOs are basically integrated development organizations with microfinance as one of their activities. These include Orangi Pilot Project, Sungi Foundation, Taraqee Foundation, Development Action for Mobilization and Emancipation (TRDP), Sindh Agricultural & Forestry Workers Coordinating Organization (SAFWCO) and Development Action for Mobilization and Emancipation (DAMEN), among others.

Khushhali Bank was established in August 2000 as part of the Government of the Islamic Republic of Pakistan's Poverty Reduction Strategy. The Pakistan Microfinance Sector Development Program (MSDP) was developed with the technical assistance and funding of the Asian Development Bank, which provided a US$150 million loan to the government of Pakistan, US$70 million being used for micro-loans provided by KB. Headquartered in Islamabad, KB operates under the central bank's supervision (State Bank of Pakistan) with several commercial banks operating as its primary shareholders.

To broaden access, there are now efforts underway to offer Shariah-compliant microfinance products to those who are reluctant to participate in interest-based banking. Farz Foundation is among the first to do so. It is engaged in Islamic micro-financing for livestock and agriculture among the rural poor.

Pakistan has a long way to go to achieve financial inclusion for the majority of its population. The current efforts on increasing access to money for the poor are a good start on a long journey that may take decades to complete. My readers who are interested in helping the poor in Pakistan by offering small loans of $25 or more have a choice of many websites to do so, including kiva.org which I have been using. The loans to Pakistani recipients are administered through Asasah, a Kiva partner in the country.

Last edited: